March 2026 Iran Special

Market Update Special

Iran Conflict: Bulls vs Bears

(3 min read)

18th March 2026

Further reading: our March 2026 article published on 3rd March 2026 “Market Rotation is Well Underway”

We are now in the third week since the start of the US/Israel war with Iran. For investors, the outlook for markets boils down to how long the conflict will go on for and in turn how long will it take to free up the Strait of Hormuz.

At the core of investor concerns will be the outlook for the oil price and the impact that will have on costs for businesses and consumers, economic growth, and inflation and how policy makers react, particularly central banks setting interest rates.

There does seem to be two clear scenarios that could unfold:

Bulls

The Bull case would see a quick end to the conflict and a downward correction in the oil price allowing the existing positive macro backdrop to resume. It is worth noting, however, that recent economic growth has disappointed to the downside, particularly in the US where Q4 GDP was revised sharply lower. A quick solution would allow markets to regain their composure allowing interest cuts to boost growth as any uptick in inflation would be regarded as transitory. A higher oil price has less of a negative impact than it did in previous oil shocks given the increased efficiency of energy usage in the overall economy.Bears

The Bear case involves the war lasting for longer and markets price for stagflation where inflation spirals higher while economic growth falters, with further disruption in global supply chains and geopolitical uncertainty escalating. Central banks would be under pressure to raise interest rates to combat inflation, and all risk assets reprice as they did in 2022. In addition, markets are digesting the stresses in private credit and uncertainties around AI. That said, markets are not pricing in any follow through to higher inflation because of the move in the oil price.

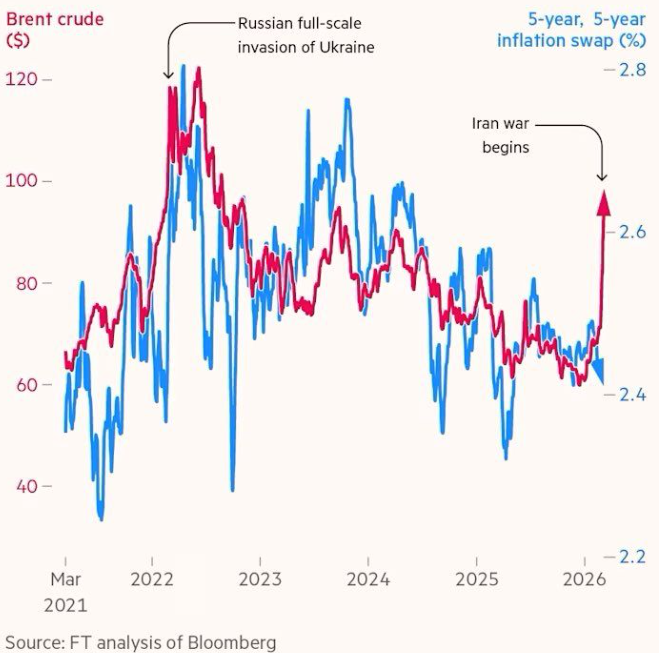

See Chart 1 below where Albert Edwards from Société Générale illustrates very well the breakdown between the oil price and the market’s future expectation for inflation.

Chart 1: Brent Crude Oil price ($) vs 5-yr inflation swap (%).

Source: FT/Bloomberg.

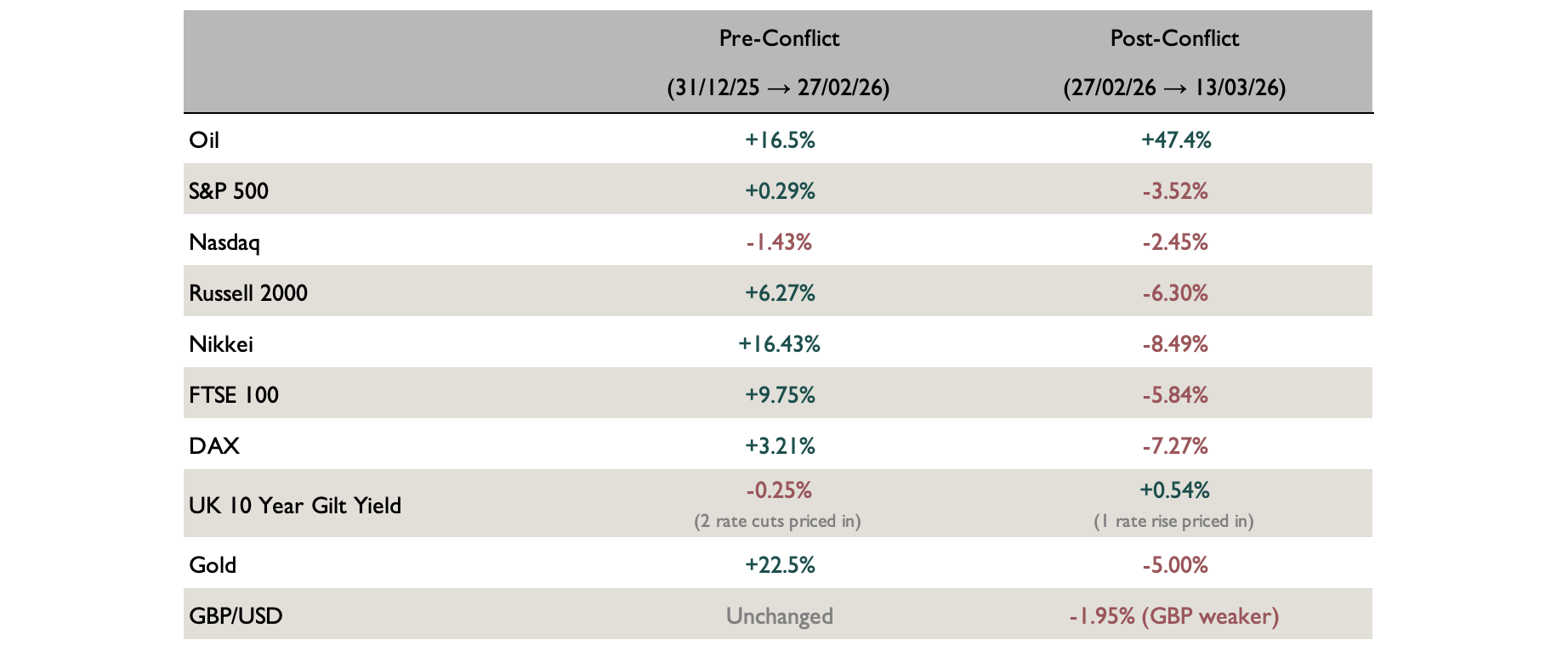

It is interesting to look at how different asset classes have performed from the beginning of the year until the conflict started and how they fared thereafter as outlined in the table below. Markets that were lagging at the start of the year such as large cap US, as investors rotated into value and small cap, have been remarkably resilient during the crisis period.

Conversely, the UK, Japan and US small cap markets which were performing well have given much of those gains back.

Chart 2: Index/asset performance pre- and post-Iran conflict (27/2/26)

Source: FE Analytics.

Gold, which one would expect to perform well during inflationary crises, has fallen since the start of the conflict. These overbought positions have clearly been sold down and, as a result, from a technical perspective are now looking much healthier.

The net outcome is that client portfolios are now unchanged on a year-to-date basis.

Providing the oil price does not spiral out of control, the long-term fundamentals for asset prices remains positive and in particular those markets that have recently benefitted from capital flows moving away from an expensive US stock market.

Peter Geikie-Cobb | Head of Investment Research

Montgomery Associates

Further Reading

Our March 2026 article published on 3rd March 2026 “Market Rotation is Well Underway”

Learn More

View our latest Factsheets and performance results for our Montgomery Portfolio Service on our Investor Information page.

Glossary

Succinct definitions of financial terms on our Glossary page.

Risk warning

This article and other articles on www.MontgomeryAssociates.co.uk does not constitute an offer or invitation in respect of investments described, nor should it be interpreted as advice or a recommendation. You should contact your financial adviser or accountant for advice relating to your circumstances. The opinions and information in this article have been prepared from sources believed to be reliable at the time and are given in good faith. The information and opinions expressed in this document represent our views at the time of preparation and may be subject to change. The value of an investment and any income from it can fall as well as rise and you may not get back the amount you originally invested.

Past performance is not a guide to future performance.

Read more Articles