October 2025

Market Commentary

Markets extend gains in the face of policy uncertainty

(4 min read)

5th October 2025

Financial markets have performed well year to date. This can be difficult to understand against a backdrop of chaotic geopolitics and a void in many areas of economic policy making globally. There was a sharp downward correction in early April 2025 due to Trump tariffs, but markets recovered quickly.

Looking at the fundamentals in the knowledge that markets do not do emotion, the economic environment could be argued as being fairly benign. Growth is positive and stable across the world, inflation is a bit above but not that far away from targets, consumer and corporate balance sheets are in good shape and high savings rates suggest that there is plenty of fire power for consumers to spend. In addition, the technological advances being made, led largely by AI, are real and this should lead to stronger trend economic growth in the future.

The main headwind is the poor state of government deficits which is likely to keep fiscal policy tight while central banks aim to keep inflation under control by maintaining interest rates higher than we have been used to in recent years.

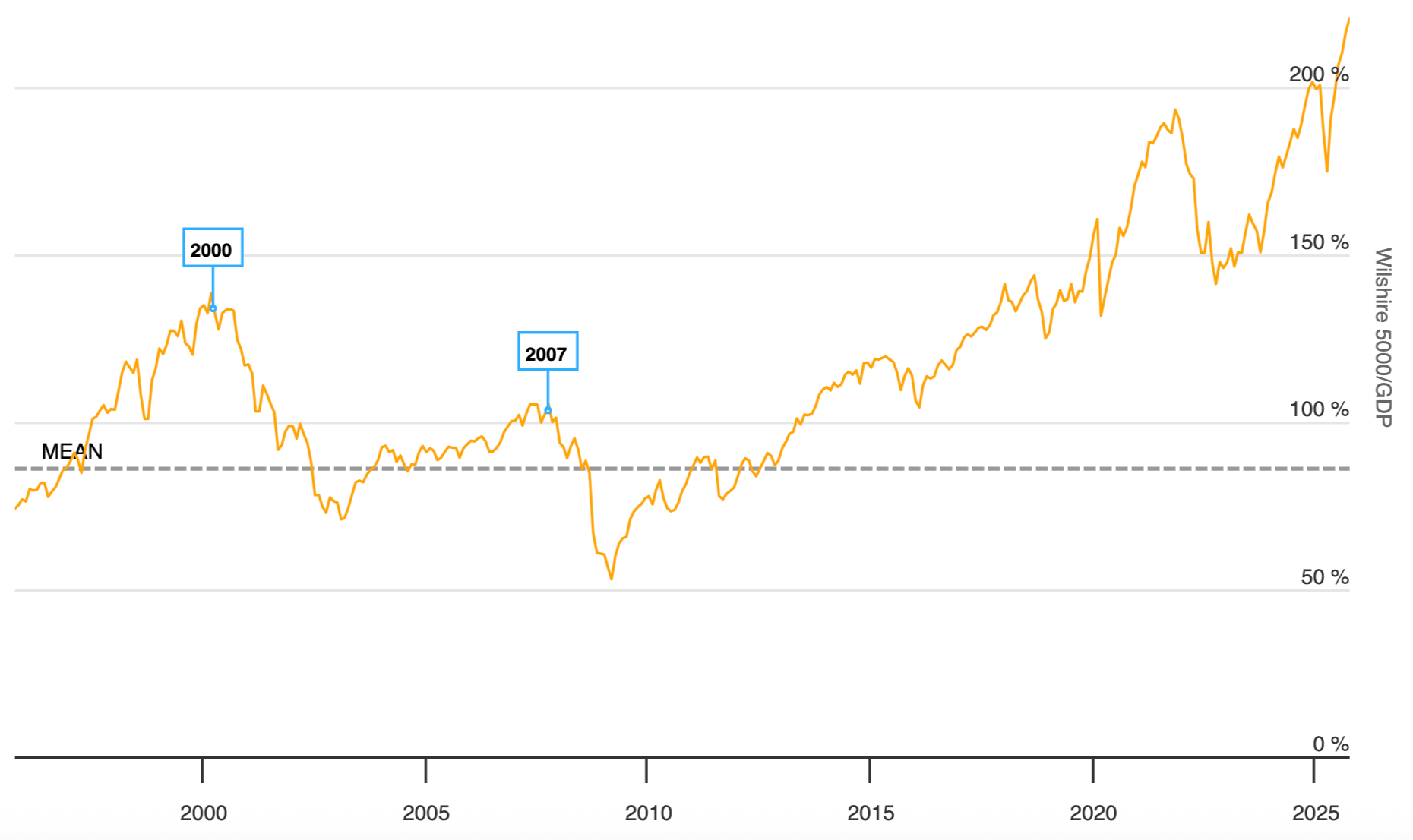

However, looking at Chart 1 below, one could be forgiven for thinking that markets have run ahead themselves. The Buffet Indicator measures the ratio of the entire value of the US market over GDP. US GDP is currently running at about $30 trillion with the capitalisation of the US stock market at approximately $65 trillion. This ratio is the highest it has been, surpassing levels seen in 2022, suggesting that the value of the stock market relative to the underlying economy is overdone. This should not be ignored but it is worth pointing out that $23 trillion out of the total $65 trillion market capitalisation is made up from the top 10 companies. In other words, there is a huge distortion due to the mega cap technology companies. We have significantly diversified client portfolios to avoid this distortion.

Chart 1: The Buffett Indicator (1995 - 2025)

US Market Cap / US GDP

Source: www.longtermtrends.net

Probably the biggest concern for investors is the uncertainty around economic policy. Chart 2 plots the UK version of the Economic Policy Uncertainty Index. The three spikes on the chart represent Brexit in 2016, the Liz Truss debacle in 2022 and Trump’s tariffs earlier this year.

If we exclude the tariff episode the index has still been at the extreme upper end of the range over the last 18 months, and this reflects two periods of policy vacuum in the UK. The first was last year following the election through to the budget in the autumn, and we are reliving this uncertainty again in the lead up to the budget at the end of November following the spending review earlier in the summer.

Businesses and consumers do not react well to long periods of uncertainty.

Chart 2: UK Economic Policy Uncertainty Index (1998-2025)

Source: www.policyuncertainty.com / www.highcharts.com

What does this mean for client portfolios?

This leads us onto how we might position portfolios for uncertainty. In February 2025 we wrote about gold and questioned its meteoric rise, increasing by 50% in the previous 12 months. Since then, over the last 7 months, the price has risen a further 34% driven primarily by central banks, particularly in the developing world, buying gold at the expense of US dollars as part of their foreign exchange reserves.

The concern that the US dollar loses its safe haven status against a background of policy uncertainty has prompted a huge buying surge for gold as the ultimate store of value.

We have maintained our weighting to gold throughout and will continue to do so while mistrust in policy makers prevails.

Peter Geikie-Cobb | Head of Investment Research

Montgomery Associates

Glossary

www.montgomeryassociates.co.uk/glossary

Risk warning

This article and other articles on www.MontgomeryAssociates.co.uk does not constitute an offer or invitation in respect of investments described, nor should it be interpreted as advice or a recommendation. You should contact your financial adviser or accountant for advice relating to your circumstances. The opinions and information in this article have been prepared from sources believed to be reliable at the time and are given in good faith. The information and opinions expressed in this document represent our views at the time of preparation and may be subject to change. The value of an investment and any income from it can fall as well as rise and you may not get back the amount you originally invested.

Past performance is not a guide to future performance.