A Fresh Look at Your Finances

New Tax Year 2026/27

(5 min read)

May 2026

Dominic Beddis | Chartered Financial Planner

The start of a new tax year is a good opportunity to take a step back and reflect on your financial position. While much of your planning may already be in place, small adjustments - particularly in a changing tax environment - can make a meaningful difference over time.

Consider the points below when reviewing your finances.

Making the Most of Your Allowances

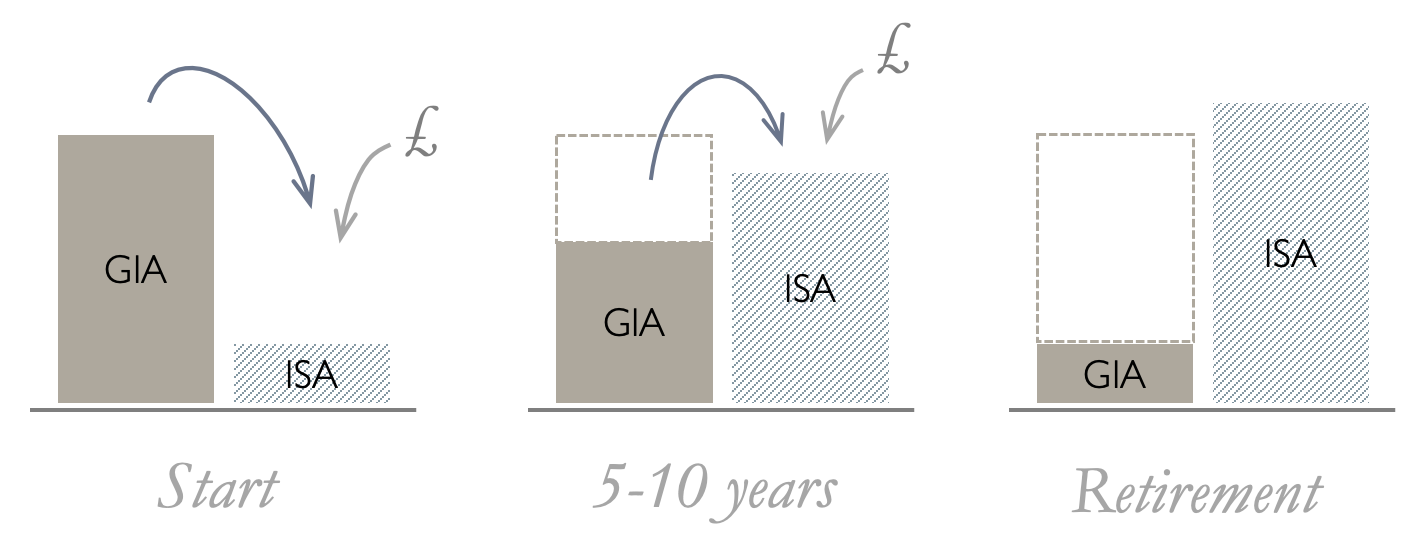

Your £20,000 ISA allowance remains one of the most valuable and straightforward ways to build wealth tax efficiently. Using your full allowance early in the tax year can allow more time for potential tax-free growth and income. For couples, this can mean up to £40,000 invested tax-efficiently each year, and by retirement you could have substantial savings in your Stocks & Shares ISA.

You could consider funding your ISA allowance either from your cash reserves, or regular top-ups from income over the course of the tax year. If you have a General Investment Account (GIA), you can raise sales from this account and use the proceeds to fund your ISA allowance - this is known as ‘Bed and ISA’. Bear in mind the tax consequences of selling investments in your GIA.

The capital gains tax (CGT) allowance (£3,000) has reduced in recent years from as high as £12,300 back in 2022/23, making it increasingly important to plan carefully when realising gains and to consider gradually moving assets into ISAs or pensions where appropriate.

If your income is around or above £100,000, your tax-free personal allowance (£12,570) may be reduced. In some cases, pension contributions can help mitigate this personal allowance tapering along with reducing your taxable income below the higher rate (£50,270) and additional rate (£125,140) income tax thresholds.

Read more about tax that applies to investments, dividends, income and savings on our Tax page.

Pensions and ISAs – Finding the Right Balance

Pensions continue to offer valuable income tax relief at your marginal rate and remain a cornerstone of long-term retirement planning, particularly for higher-rate taxpayers.

Taking account of the tax incentives for a pension during the accumulation phase (while working) and decumulation phase (retirement), the ‘net’ return will normally be greater by saving into a pension when compared with an ISA. There are numerous factors that can affect this outcome however, such as investment performance, fees and charges, maximising contributions, the level of your earnings and so on.

For example, a gross pension contribution of £16,667 would cost a higher rate taxpayer £10,000. Ignoring growth, the return when withdrawn in retirement, even if the individual is still a 40% taxpayer, is £11,667 (£7,500 income after tax plus £4,167 tax-free cash). The same £10,000 invested in an ISA will still be £10,000 when taken. The spendable pot from the pension after all taxes is therefore 17% more than an ISA, simply because of the tax treatment.

Had the same individual only been a basic rate taxpayer when drawing their pension, the net return would increase to £14,167, an increase of 41% on the ISA.

Pensions remain valuable but since inheritance tax rules on pensions are changing in April 2027, the strategy has shifted from ‘preserve for inheritance’ to a more balanced approach between funding retirement and managing future tax exposure.

ISAs, while not offering upfront tax relief, provide flexibility and tax-free access to funds, which can be especially useful before pension access age or for unplanned needs.

For many investors, a combination of both provides a balanced and flexible approach.

Finding the balance

For many investors, a combination of an ISA, General Investment Account (GIA) and a Pension often provides a balanced and flexible approach.

Looking ahead: pension changes from April 2027

First announced in the 2024 Autumn Budget, it is expected that untouched/undrawn personal pensions will form part of your estate for inheritance tax purposes from April 2027. This represents an important shift and may mean that pensions are less effective as a tool for passing on wealth.

It may be appropriate to review whether to draw on pension funds earlier than previously planned to move this money into a more inheritance tax efficient strategy. Ensuring beneficiary nominations are up to date remains essential.

Estate Planning and Passing on Wealth

Inheritance tax thresholds remain frozen which may gradually bring more estates into scope over time. There is a growing shift in mindset of passing on wealth during your lifetime, not just on death.

There are still valuable opportunities to pass on wealth inheritance tax-efficiently:

The £3,000 annual gifting allowance can be used each year.

Larger gifts may fall outside your estate after seven years.

Regular gifts from excess income can be particularly effective when structured correctly.

Trusts and other planning structures may also be appropriate depending on your circumstances and objectives.

Supporting the Next Generation

Many clients are increasingly choosing to pass on wealth earlier, often at a stage where it can have the greatest impact - such as supporting property purchases or education costs.

Funding Junior ISAs (£9,000 allowance) and pensions for children can also form part of a long-term family wealth strategy, and open conversations with family members can help ensure your intentions are understood and support effective long-term planning.

Montgomery Wealth - coming Summer 2026

We are excited to be launching a new service soon designed specifically for the rising generation of clients and their family members. These accounts can be opened by an adult either for themselves or for a child with three ready-made Montgomery portfolios to choose from. It’s straightforward and will allow for easy gifting to younger generations.

Join the mailing list to be the first to hear when it launches: https://www.montgomerywealth.co.uk/

Structuring Your Investments Thoughtfully

The way investments are structured can be just as important as the investments themselves. Holding assets in the most appropriate tax ‘wrapper’ can improve long-term outcomes.

Depending on your circumstances, additional structures such as investment bonds (onshore/offshore) may also be worth considering as part of a broader strategy where tax deferral or estate planning are a priority.

A final thought

The tax landscape continues to evolve and even small adjustments can have a meaningful impact over time. Financial planning becomes less about single decisions and more about coordination by aligning tax efficiency, investment strategy, and long-term family objectives.

As you reflect on the year ahead, consider:

Are you making full use of available allowances?

Is your current balance between pensions, ISAs and GIAs still appropriate?

Have you reviewed how your wealth might be passed on in light of inheritance tax changes?

Dominic Beddis | Chartered Financial Planner

Montgomery Associates

Dominic Beddis FPFS

HEAD OF INVESTMENTS & FINANCIAL PLANNING

Dominic is a Chartered Financial Planner and advises on investments and broader finance, helping clients to make their wealth work for them by protecting and growing the assets they have and ensuring they save and invest tax-efficiently.

Further Reading

See our Tax page for insights into the changes announced at the Autumn Budgets in 2024 and 2025.

Learn More

Launching Summer 2026: Montgomery Wealth is dedicated to the next generation of investors, those building their career, climbing the property ladder or raising a family. Join the Montgomery Wealth mailing list to be the first to hear.

Glossary

Succinct definitions of financial terms on our Glossary page.

Risk warning

This article and other articles on www.MontgomeryAssociates.co.uk do not constitute an offer or invitation in respect of investments described, nor should it be interpreted as advice or a recommendation. You should contact your financial adviser or accountant for advice relating to your circumstances. The opinions and information in this article have been prepared from sources believed to be reliable at the time and are given in good faith. The information and opinions expressed in this document represent our views at the time of preparation and may be subject to change. The value of an investment and any income from it can fall as well as rise and you may not get back the amount you originally invested.

Past performance is not a guide to future performance.

Read more Articles