June 2025

Market Commentary

A US Economy in Equilibrium

(3 min read)

4th June 2025

Unlike the Bank of England which has a single mandate to target inflation at 2%, the US Federal Reserve’s (Fed) remit is to achieve price stability, 2% inflation, and full employment.

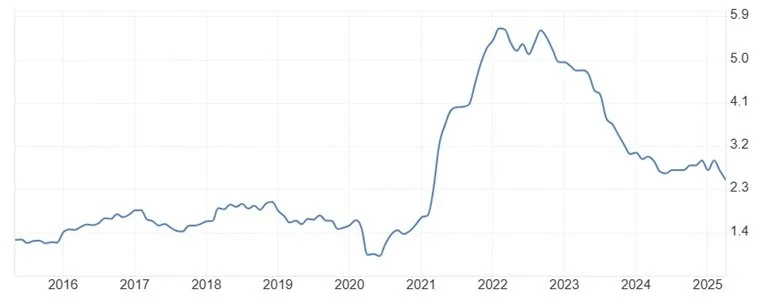

Amongst all the chaotic political backdrop including supranational entities such as the World Bank, the IMF and the OECD adjusting economic forecasts in an attempt to factor in every piece of government policy makers’ rhetoric, the two main goals of the Fed seem unusually in equilibrium. The preferred measure of inflation for the Fed is the Core PCE Price Index which currently stands at 2.5% with a target of 2%.

The level of inflation, which has been coming down consistently from uncomfortable levels caused by supply chain problems because of the war in Ukraine, was rather sticky a year ago but now looks to be trending down to within the Fed’s comfort zone.

Two conflicting factors are driving inflation:

inflationary pressures stemming from higher wages, supply chain uncertainties and tariffs

deflationary forces caused by continued advances in technology including AI with the speed of these changes increasing all the time. Nvidia’s recent results continue to demonstrate this.

The result should produce a more stable aggregate inflation outlook.

Chart 1

US Core PCE Price Index Annual Change

Source: US Bureau of Economic Analysis

The second component of the Fed’s mandate, full employment, also appears close to target. The current Non-Accelerating Inflation Rate of Unemployment (NAIRU) in the US is currently estimated to be around 4%, with the most recent level at 4.2%. Although dropping recently, there are still 7.2 million job openings in the US suggesting the labour market remains robust. With the Fed’s dual mandate currently at target it is unlikely we should expect significant moves in US interest rates unless there is an unforeseen event. Some stability in rates might not be a bad thing in a world full of uncertain headlines.

What does this mean for client portfolios?

The implication for investors is that shorter dated fixed income should compliment stocks with strong balance sheets producing decent cashflow. It will be the indebted entities that suffer during this environment of 2%+ real interest rates as quality assets will significantly outperform.

These factors are at the core of our client portfolios.

Peter Geikie-Cobb | Head of Investment Research

Montgomery Associates

Glossary

www.montgomeryassociates.co.uk/glossary

Risk warning

This article and other articles on www.MontgomeryAssociates.co.uk does not constitute an offer or invitation in respect of investments described, nor should it be interpreted as advice or a recommendation. You should contact your financial adviser or accountant for advice relating to your circumstances. The opinions and information in this article have been prepared from sources believed to be reliable at the time and are given in good faith. The information and opinions expressed in this document represent our views at the time of preparation and may be subject to change. The value of an investment and any income from it can fall as well as rise and you may not get back the amount you originally invested.

Past performance is not a guide to future performance.