March 2025

Market Commentary

The Importance of Diversification

(4 min read)

7th March 2025

The start of 2025 has been testing as investors try to digest the news flow, dominated by politics, and what it all means for the global economy and markets. One comment doing the rounds again is that we should take President Trump seriously but not literally, but recent events suggest we cannot be complacent on the literally part of that assessment.

When making asset allocation decisions we try to set out a series of plausible scenarios and attach probabilities to potential outcomes. The world order in recent weeks has changed significantly: the US will no longer subsidise European security. This will potentially have huge economic implications and impact the performance of sectors within the global stock market.

The macro-outlook seems binary. A prolonged war in Ukraine combined with permanent US tariffs would imply a world dominated by stagflationary pressures, slowing trade, higher prices and elevated commodity prices exasperating the cost-of-living crisis. On the other hand, a peace deal - combined with a resolution to the trade imbalance the US has with the rest of the world and a commitment from Europe to fund its own security, and it looks as though Germany is ready to do this in size - could ignite strong, low inflationary growth globally.

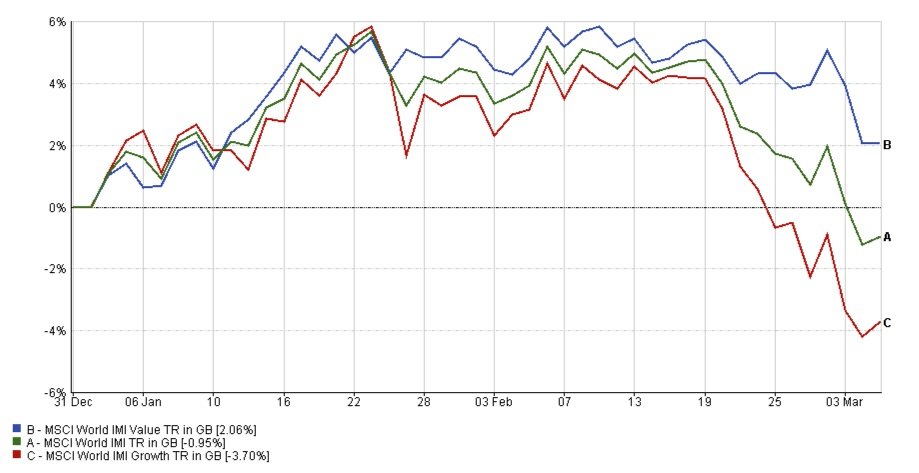

We cannot predict the outcome, but we can try and prepare for different possibilities. Last year global markets were driven by a strong but narrow performance of the ‘Magnificent 7’ mega cap US technology stocks and ‘value’ or more defensive sectors and stocks were left behind. So far this year the reverse has happened. Technology and ‘growth’ stocks have suffered a significant correction for a variety of reasons - rich valuations and higher-for-longer interest rates due to sticky inflation, while we have seen a rotation into ‘value’ or defensive stocks. See chart below.

Chart

MSCI world indices year to date performance: value versus growth.

Chart range: 31/12/24 - 5/3/25

Source: FE Fundinfo

What does this mean for clients?

As a result of all this uncertainty at the headline level, the strategy of robust diversification in our client portfolios has never been more important, across asset classes and sectors and styles within equity markets. To summarise our investment strategy for moderate risk client portfolios at top-down level, we have three main components that make up that strategy, all serving different roles and ready to contribute during varying market environments.

First, there is the growth component, roughly 30%, which is made up of strong thematic and secular trends with long-term growth prospects such as technology, emerging markets with excellent fundamentals, and smaller companies. This component of portfolios will have high risk and reward characteristics with above-market volatility.

To reduce this volatility, we have the second component, about 40%, which invests in defensive, value and income investments with solid long-term companies with strong balance sheets and dividend cover. In addition, we have decent exposure to the UK market which is cheap and undervalued relative to its own history and versus other global markets.

Finally, the third component, roughly 30%, comprising market-neutral equity funds which take advantage of relative value opportunities, but without having exposure to the direction of the market, and bonds which currently yield about 5% and would benefit from interest rate cuts against a background of slower economic growth.

Although we are only two months into the new year, it has been eventful. At the time of writing, client portfolios are slightly up versus global markets being slightly down while, as the chart above illustrates, the performance between ‘value’ and ‘growth’ has been starkly different.

As we have commented in the past, the headlines can make grim reading but if we can ignore much of the noise there are always opportunities to pursue while diversification reduces the bumps in the road.

Peter Geikie-Cobb | Head of Investment Research

Montgomery Associates

Glossary

www.montgomeryassociates.co.uk/glossary

Risk warning

This article and other articles on www.MontgomeryAssociates.co.uk does not constitute an offer or invitation in respect of investments described, nor should it be interpreted as advice or a recommendation. You should contact your financial adviser or accountant for advice relating to your circumstances. The opinions and information in this article have been prepared from sources believed to be reliable at the time and are given in good faith. The information and opinions expressed in this document represent our views at the time of preparation and may be subject to change. The value of an investment and any income from it can fall as well as rise and you may not get back the amount you originally invested. Past performance is not a guide to future performance.