October 2023

Market Commentary

Higher for longer

(3 min read)

There has been a lot of commentary recently on the sharp rise in long term interest rates priced into the government bond markets. In the US and UK central banks have had to be aggressive in raising interest from zero to 5% over the last 18 months to try and regain credibility when it comes to their inflation mandates. Over that period all asset classes have had to adjust to the new ‘risk free’ rates –the interest rate you can enjoy without having to take any risk, such as a government-backed savings account. However, markets, and particularly longer dated bonds, began to discount the prospect of interest rate cuts in 2024 as inflation falls closer to target and the likelihood of a recession increased.

In recent trading days sharp price swings in the bond market have put pressure on all asset classes again due to the resilience of the US economy, as the continued tight employment market supports the consumer and leads to the possible need for central banks to continue to raise interest rates to further fight sticky inflation. The consensus, therefore, had thought that we were close to or at the peak of the interest rates cycle. Federal Reserve and Bank of England officials have recently poured cold water on the view that cuts in interest rates can be expected in the first half of next year and have brought the market to heel by implying that there could be further rises ahead but that, in any event, policy will be held at current levels for longer.

Our view is that we are close to the peak of the interest rate cycle even if further rises are likely but, given the shift in global themes surrounding demographics, climate change and deglobalisation which lead to a more stubborn nature of inflation, we think interest rates will remain at or near current levels for some time. Assets that require easier policy to perform will be disappointed but there are plenty of companies with strong balance sheets that will not only cope with this environment but could also thrive.

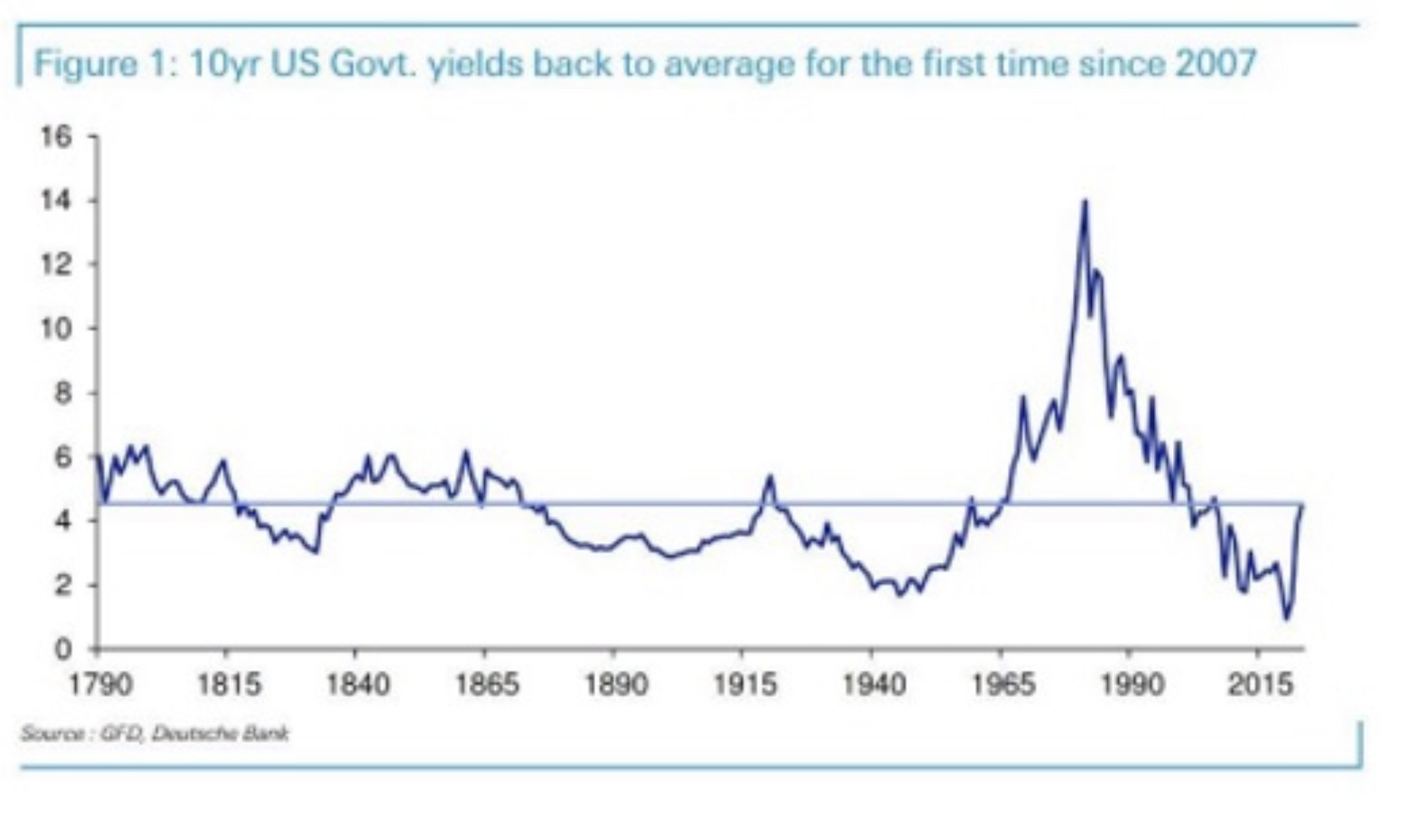

As the chart below from a recent Deutsche Bank study illustrates, current bond yields are back to their long-term average. While still having a low allocation to fixed interest, we have increased our exposure recently but focused on shorter maturities with lower capital risk. Any further bond market sell off will provide a good opportunity to increase the weighting and lock in attractive long-term returns.

Peter Geikie-Cobb | Head of Investment Research

Montgomery Associates

5th October 2023