February 2026

Market Update

Fool’s Gold

(4 min read)

4th February 2026

The sharp rise and fall of the gold price in recent days was clearly fuelled by speculative flows. However, given the potential for geopolitical and economic policy errors in the US, gold should still remain a core holding in portfolios.

It has been an eventful start to the year for financial markets. The major equity indices are in positive territory but accompanied by the usual volatility surrounding earnings season, with the focus on AI capital expenditure, and the remarkable geopolitical rhetoric we have become used to.

The Vix Index - a measure of ‘fear’ and volatility for the S&P 500 - increased from 14 to 20, not as high as levels seen last year but enough to worry shaky investors. Bond markets have been unusually stable, except in Japan where the central bank is normalising monetary policy. The UK gilt market, for now at least, seems more sanguine about the government deficit. Foreign exchange markets continue to focus on a weaker US Dollar as investors and Emerging Market central banks consider diversifying away from the world’s reserve currency.

Commodities

The main area of note so far this year, however, has been in commodity prices with the Goldman Sachs Commodity Index increasing by over 6%. Energy prices have increased although remain stable given the continued uncertainty in the Middle East with President Trump’s threat to Iran and intervention in Venezuela. The big move has been in metals, particularly copper, silver, and gold. Copper is driven by the outlook for economic activity, as is silver due to its industrial use and as an alternative to gold.

Gold

Gold, however, seems to have stolen the headlines. After an impressive return of circa 65% in 2025 it continues to power ahead year to date, increasing by over 23% at its peak before retreating to a positive performance of 13% at the time of writing (see Chart 1 below). It is impossible to value gold in the same way as you can use a yield for bonds and earnings growth for equities to judge historical and absolute valuations. We can measure historical price ratios relative to other commodities such as silver but the overall demand dynamics will be different.

There is no doubt that gold’s very recent price action was overdone. It normally is when it becomes the Uber driver’s preferred topic of conversation.

Chart 1

Gold price in Dollars/oz

over 12 months. Current price $4,921/oz at the time of writing.

Source: Google Finance

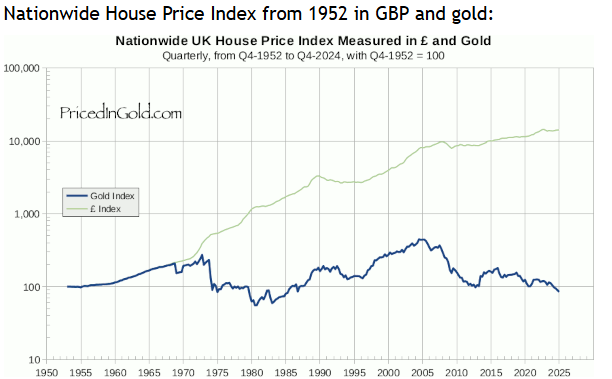

Gold should be viewed as a long-term store of value which is very difficult to trade. Chart 2 below demonstrates this very well. When measured in GBP, UK house prices have increased over 100 times since the early 1950s but measured in gold terms house prices are about the same as in 1952! Since 2005, house prices have risen by almost 50% while in gold terms they have fallen 75%.

Chart 2

Nationwide House Price Index measured in £ and Gold

(1952 - 2024)

Source: https://pricedingold.com/

It is unlikely the US Dollar will lose its status as the world’s reserve currency soon. However, it is worth noting a few points that could undermine this view. President Trump seems very content to talk the currency down to gain competitiveness versus major trading partners. He has also been disruptive in undermining the independence of the Federal Reserve and its inflation credibility.

In addition, investors questioning US exceptionalism, renewed US policy uncertainty and a government deficit that is unsustainable in the longer term can only increase the potential for diversification into gold as that store of value.

Unless the macro backdrop changes dramatically, a position in client portfolios should be maintained.

Peter Geikie-Cobb | Head of Investment Research

Montgomery Associates

Further Reading

See our past articles on the topic of gold in February 2025, October 2025 and November 2025.

Learn More

View our latest Factsheets and performance results for our Montgomery Portfolio Service on our Investor Information page.

Glossary

Succinct definitions of financial terms on our Glossary page.

Risk warning

This article and other articles on www.MontgomeryAssociates.co.uk does not constitute an offer or invitation in respect of investments described, nor should it be interpreted as advice or a recommendation. You should contact your financial adviser or accountant for advice relating to your circumstances. The opinions and information in this article have been prepared from sources believed to be reliable at the time and are given in good faith. The information and opinions expressed in this document represent our views at the time of preparation and may be subject to change. The value of an investment and any income from it can fall as well as rise and you may not get back the amount you originally invested.

Past performance is not a guide to future performance.

Read more Articles