January 2026

Market Update

Geopolitical Strain vs Macro Optimism

(4 min read)

15th January 2026

As 2026 gets underway, the somewhat bizarre theme of alarming geopolitical headlines combined with a promising macro-economic outlook and exciting investment opportunities continues.

Recent headlines around the US, Venezuela and Greenland are, of course, very concerning but markets are not driven by political emotions. They are driven by the economic outlook and financial returns of companies.

The US intervention on Venezuela has had, albeit in the very short term, a positive response from markets mainly due to the view that President Trump is doing everything he can to keep the oil price down, in turn reducing input costs for businesses and consumers. The possibility of lower inflation should reduce or keep interest rates at current stimulative levels.

There is no room for complacency and there are plenty of issues to be wary of but, for now, the geopolitical backdrop, as we experienced last year, does not appear to be a major driver for markets.

Tech and AI

Last year saw some impressive returns from technology stocks, which we had good exposure to, driven by the AI theme. There has been much debate on whether a repeat of the Dot Com bubble bursting is just around the corner. Certainly, stock valuations of the US mega cap Magnificent Seven would justify having sympathy with this view.

On the other hand, all last year’s AI capex (capital expenditure) came from corporate free cashflow - a very different situation from the leverage of the Dot Com mania in 2000. However, there are some warning signs. In the fourth quarter of last year, the mega cap companies did start to issue debt to raise funds for AI investment and indeed Oracle bonds, rather unfairly in my view, are trading at junk levels*. Maybe the bond market is giving the equity market a signal. The proof of the robustness of the AI theme will be tested as Anthropic, Open AI and Space X come to market with their planned Initial Public Offerings (IPO) later this year.

* A bond labelled as ‘junk’ is considered to be higher risk or sub-investment grade owing to its heightened chance of default/failure, however it can carry the benefit of producing a more generous income or ‘yield’.

US

However, we have already seen some significant rotation in terms of market performance away from the US, and particularly from the technology sector. 70% of non-US markets outperformed the S&P500 and there was noticeable rotation and broadening within the US market too. We have been positioned for this and mentioned in previous notes the importance of diversification for a shift in market leadership (see articles from March 2025 and November 2025: “The Importance of Diversification” and “Diversification Delivers”).

Montgomery strategy

We continue to follow this strategy and have decent exposure to small and medium cap investments in the UK and globally, as well as significant weightings to value stocks which sit comfortably along side our exposure to large and mega cap growth and technology companies. Gold and fixed income are also in portfolios in the event of equity market shocks.

As we digest all the risks for markets, we should not forget that the macro-economic and policy backdrop remains supportive. Having dealt with significant monetary tightening in 2022/23 in the form of higher interest rates, the global economy is enjoying strong tailwinds as central banks have and are likely to continue cutting interest rates while simultaneously governments keep the fiscal taps flowing.

What does this mean for client portfolios?

Our strategy remains broadly unchanged as we start the New Year. We are excited about the technological revolution that is happening in the form of AI and the impact it will have on future productivity and growth and remain positioned to take advantage of this theme.

However, we realise that anomalies in terms of relative valuations within markets have risen and diversification in portfolios is taking full advantage of this. Fixed Income at the shorter and medium maturities remain a good back stop for reducing volatility along the way.

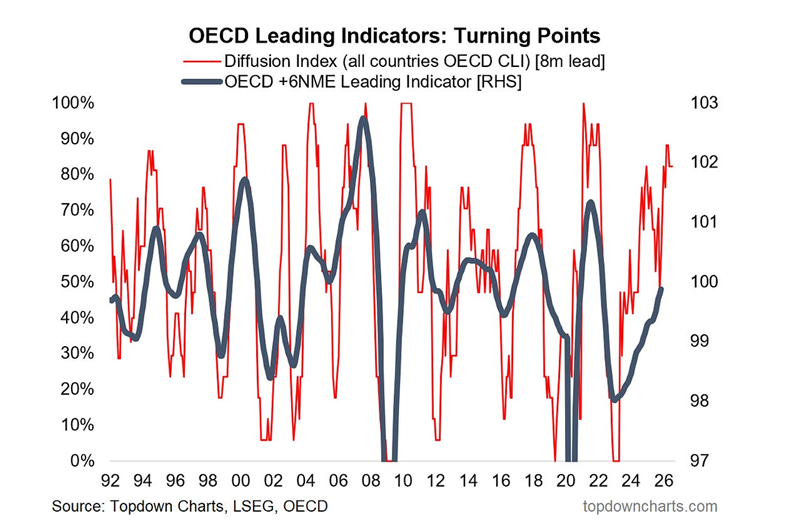

OECD Leading Indicators: Turning Points

Source: Topdown Charts, LSEG, OECD (Organisation for Economic Co-operation and Development)

The chart above plots leading indicators for the growth outlook in the OECD (Organisation for Economic Co-operation and Development), and this suggests that with government spending and further increases in investment, corporate profits and overall growth will remain solid. Stubborn inflation is the main issue for central banks and the path to lower interest rates.

Peter Geikie-Cobb | Head of Investment Research

Montgomery Associates

Further Reading

Read our recent article ‘Diversification Delivers’ from 5th November 2025 which interrogates what has driven our portfolio’s returns in 2025.

Learn More

View our latest Factsheets and performance results for our Montgomery Portfolio Service on our Investor Information page.

Glossary

Succinct definitions of financial terms on our Glossary page.

Risk warning

This article and other articles on www.MontgomeryAssociates.co.uk does not constitute an offer or invitation in respect of investments described, nor should it be interpreted as advice or a recommendation. You should contact your financial adviser or accountant for advice relating to your circumstances. The opinions and information in this article have been prepared from sources believed to be reliable at the time and are given in good faith. The information and opinions expressed in this document represent our views at the time of preparation and may be subject to change. The value of an investment and any income from it can fall as well as rise and you may not get back the amount you originally invested.

Past performance is not a guide to future performance.

Read more Articles